As Rates Rise, Investment Strategies Must Meet IMR Challenges

March 21, 2023

By Jeremy Lachtrupp, Managing Director, Insurance Solutions and Matt Reilly, Managing Director, Insurance Solutions

The recent turn upward in interest rates has been long-awaited by life insurers, but it also poses portfolio management challenges as realizing losses could negatively impact balance sheet strength. The Interest Maintenance Reserve (IMR), a 30-year-old accounting standard, has helped smooth insurers’ annual income amid changing market conditions but has never seen an extended period of rising interest rates. And as rates are expected to keep increasing, the impact on IMR could harm insurers’ capital and income.

When rates were falling, many insurers saw growth in their IMR balances due to gains from the sale of bonds prior to maturity; the gains were eventually amortized from the IMR into net investment income (NII) over the remaining life of the sold asset. As rates rose in 2022 however, the opposite dynamic took effect: insurers experienced losses from selling lower-yielding bonds to replace them with higher-yielding ones, leading to declines in IMRs and a likely drag in future NII. Many insurers risk their IMR balances shrinking further or even turning negative should they continue to sell bonds in pursuit of higher yields.

However, statutory accounting rules treat negative IMR as a non-admitted asset so IMR values below zero fall directly to capital and surplus, reducing the value of these critical financial health measures. Yes, insurers could look weaker even as their portfolios may be generating greater yields. The ACLI has petitioned the NAIC to adjust how statutory accounting treats negative IMR, but for now the rule stands.

A desire to avoid having negative IMR may make insurers increasingly reluctant to trade as they seek to minimize losses and even forgo opportunities that could benefit their long-term economic value. It has become abundantly clear that accounting for IMR is now a vital constraint that insurers must incorporate when managing their portfolios and setting investment strategy, adding another level of complexity to the process.

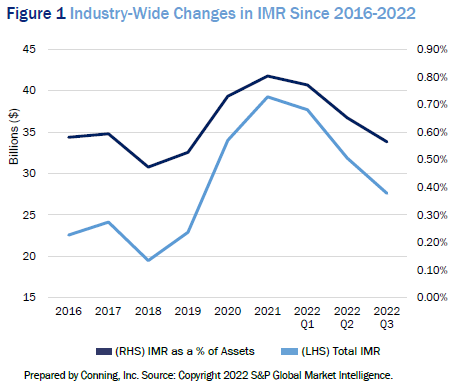

Steady Growth in IMR Balances Reversed in 2022

Aggregate IMR for the U.S. life insurance industry more than doubled between 2018 and 2021, from $19.5 billion in 2018 to $39.3 billion (see Figure 1). This increase isn’t simply the result of a growing asset book: the percentage of IMR relative to net admitted assets increased to 80 basis points from 47 during that same period.

The 2022 spike in interest rates significantly disrupted the historical trend and many insurers face the prospect of a negative IMR balance. The economic offset that IMR provides to the right side of the balance sheet will no longer be available if the current Statutory Accounting Principle (SAP) guidance continues to disallow the admittance of aggregate negative IMR.

Click below to continue reading Conning’s Viewpoint, “As Rates Rise, Investment Strategies Must Meet IMR Challenges."

Disclosure

Past performance is not a guarantee of future results.

©2023 Conning, Inc. All rights reserved. The information herein is proprietary to Conning, and represents the opinion of Conning. No part of the information above may be distributed, reproduced, transcribed, transmitted, stored in an electronic retrieval system or translated into any language in any form by any means without the prior written permission of Conning. This publication is intended only to inform readers about general developments of interest and does not constitute investment advice. The information contained herein is not guaranteed. to be complete or accurate and Conning cannot be held liable for any errors in or any reliance upon this information. Any opinions contained herein are subject to change without notice. Conning, Inc., Goodwin Capital Advisers, Inc., Conning Investment Products, Inc., a FINRA-registered broker-dealer, Conning Asset Management Limited, Conning Asia Pacific Limited, Octagon Credit Investors, LLC and Global Evolution Holding ApS and its group of companies are all direct or indirect subsidiaries of Conning Holdings Limited (collectively “Conning”) which is one of the family of companies owned by Cathay Financial Holding Co., Ltd. a Taiwan-based company. C: 16574250